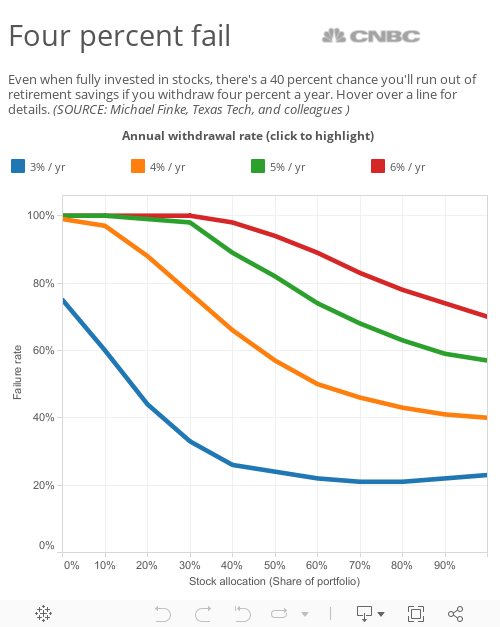

For years, financial advisors have tried to keep retirement planning simple. You can count on the stock market returning roughly 7 percent a year over the long run, according to the conventional wisdom, and expect to withdraw about 4 percent from your nest egg every year once you're retired.

Unfortunately, those two little numbers just don't add up any more. This week, one of our readers asks why. (Tweet This)

Please explain, when the stock market has earned an [average annual] return in the range of 7 percent over the long term, how a 4 percent withdrawal rate from a retirement fund will exhaust funds in about 30 years. It must be related to the fluctuations coupled with the steady annual withdrawal. — Perry W.

It sounds like the math should work: if you can get a 7 percent return over the long term and you're only withdrawing 4 percent, why wouldn't your savings last forever? Unfortunately, the conventional wisdom overlooks two big problems with that assumption. Let's take the 7 percent return first.

Got a question about business or personal finance?

Send it along to Explains@cnbc.com

Every week, the world of business and finance brings news that seems designed to confuse most of us. So CNBC Explains wants to hear from you. Each week, we'll answer as many of your questions as we can. (Like most readers, we'd also like to know your first name and where you're from. We may also edit your questions for space.) Any question is fair game.

It's true that, when you average out the stock market's ups and downs, the investment return for the Standard & Poor's 500 index over the long term (back to 1928) has been about 7.5 percent. Adjusted for inflation, though, that long-term return has been more like 4.4 percent. Add back in the return from reinvesting dividends, adjust for inflation again and the return goes back up to 8.6 percent. (We're using a simple compound average. Your estimates may vary.)

Those long-term averages help explain why it's a good idea to invest in stocks if you're young and have a long time to build up your retirement savings. If the market drops, you still have plenty of time to make up those losses in good years. (The simplest way is with a low-cost index fund; if you invest in a managed fund, you will typically pay more in investment fees. Compounded over decades, those fees add up.)

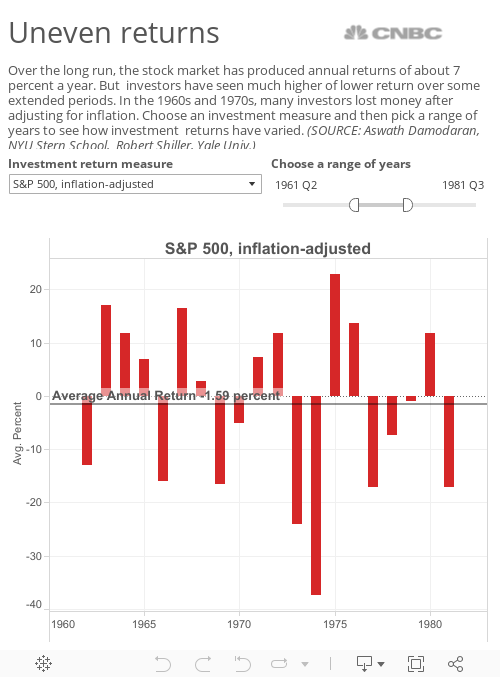

But once you're retired, your horizon shrinks considerably, so you may not have time to make up for those down years—especially if the stock market hits a lengthy slump. There have been plenty of 10-year periods when average annual returns were much less than the long-term average. During the 1960s and 1970s, for example, the inflation-adjusted S&P 500 index fell by an average 1.6 percent a year. So your nest egg would have shrunk even if you'd made no withdrawals at all.