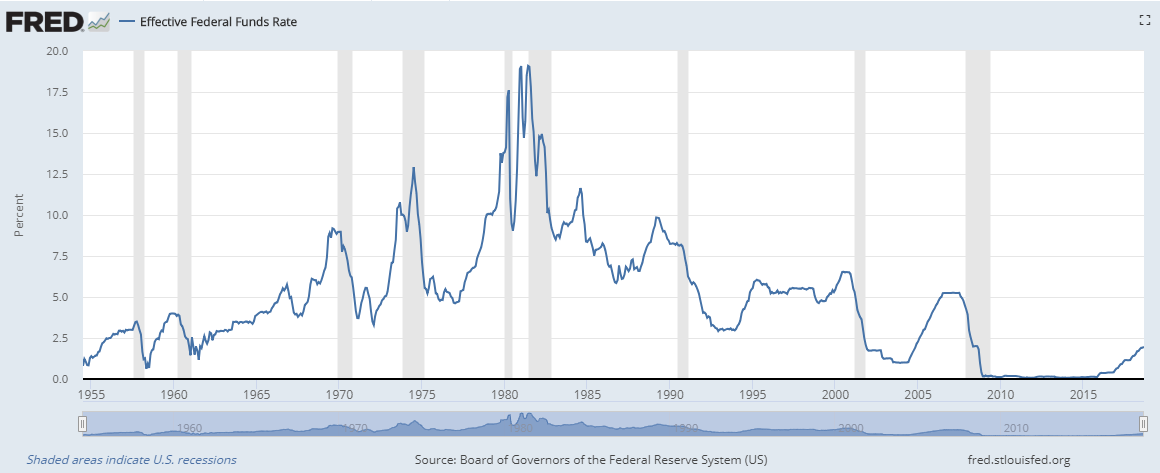

The effective Federal Funds rate (the rate set by the Federal Reserve which is what banks charge to lend each other money overnight) is presently 2.18 percent. The average Federal Funds rate from 2000 to 2015, before the Federal Reserve began raising rates, was 1.71 percent. Shockingly from 2000 to the present, the Federal Funds rate was lower than the current rate of 2.18 percent, an estimated 73 percent of the time.

The pundits at the Federal Reserve indicate that the agency is striving to raise interest rates to a "neutral rate." Observers believe that this would be in the 3.25 percent to 3.50 percent range. The history of the Federal Funds rate in the last 18 years does not indicate that it ever stabilized at anywhere near this rate. The average Federal Funds rate since it was first published in July 1954 has been 4.80 percent.

It would appear that the Fed simply made up this concept of a "neutral rate" since there is little evidence that it has ever existed before. Interestingly, CNBC's Andrew Ross Sorkin recently interviewed ex Fed Chairman Paul Volcker. In the interview Mr. Volcker stated "a 2 percent [inflation] target, or limit, was not in my textbook years ago. I know of no theoretical justification."

Apparently, Mr. Volcker thinks that the Fed may have made up the 2 percent number as a convenience. Others may think that the "neutral rate" concept was conceived for similar reasons.

The Federal Reserve is shrinking its balance sheet at the fastest rate recorded since it began publishing these numbers in 2002. In the past 12 months since it began shrinking, assets are down by $262 billion or 6.3 percent.